Change fuelled by digital transformation and the data revolution.

In its inaugural Voice of the Enterprise (VotE) Digital Pulse survey, 451 Research finds that IT leaders are embracing a new model of off-premises, service-oriented IT solutions and will be looking to harness data in new ways to differentiate themselves in 2018. Respondents revealed that the top three IT initiatives for 2018 are all data-centric: business intelligence, machine learning/artificial intelligence and big data.

The survey finds that IT organizations’ ability to exploit digital transformation is uneven with over 60% of organizations having no formal transformation strategy in place and many admitting they face challenges in achieving optimal business-IT alignment.

Sixty percent of enterprises surveyed for Digital Pulse say they will run the majority of their IT outside the confines of enterprise datacenters by the end of 2019, chiefly using off-premises service provider environments such as public cloud infrastructure and SaaS.

Accordingly, the largest spending increase in 2018 is for IT delivered ‘as a service,’ at the expense of the traditional on-premises model. 451 Research finds information security is also high on the IT agenda, with 16% of organizations saying that area is getting the largest budget increase.

Providers such as Microsoft and Amazon Web Services (AWS) are emerging as enterprises’ most strategic technology suppliers; 35% of organizations say Microsoft will be their most strategic partner by the end of 2019, compared to 33% today, while 17% say AWS will hold that position two years from now compared to 7% today.

The Digital Pulse survey also highlights a revolution in how organizations will harness data to differentiate themselves and create new value. The top three IT initiatives for 2018 were all data-centric: 45% of respondents pointed to business intelligence, 29% mentioned machine learning/artificial intelligence while 28% said big data.

The growth opportunity around data is clear with almost 30% of organizations saying ML/AI is a top priority in 2018 while just 12% of respondents use these solutions today.

Meanwhile, usage of much-hyped technologies such as blockchain remains very low, but more organizations will begin to move from tire kicking to actual deployment over the next year, with 12% of Digital Pulse respondents citing blockchain as a top IT priority for 2018.

“The survey suggests that many – but certainly not all – organizations are finally reaching the point where they can focus on endeavors that help differentiate the business, instead of merely keeping the lights on. In 2018 we expect to see much of this effort focused around a new set of approaches to data optimization and analysis,” said Melanie Posey, Research Vice President and General Manager, Voice of the Enterprise, 451 Research.

Worldwide IT spending is projected to total $3.7 trillion in 2018, an increase of 4.5 percent from 2017, according to the latest forecast by Gartner, Inc.

"Global IT spending growth began to turn around in 2017, with continued growth expected over the next few years. However, uncertainty looms as organizations consider the potential impacts of Brexit, currency fluctuations, and a possible global recession," said John-David Lovelock, research vice president at Gartner. "Despite this uncertainty, businesses will continue to invest in IT as they anticipate revenue growth, but their spending patterns will shift. Projects in digital business, blockchain, Internet of Things (IoT), and progression from big data to algorithms to machine learning to artificial intelligence (AI) will continue to be main drivers of growth."

Enterprise software continues to exhibit strong growth, with worldwide software spending projected to grow 9.5 percent in 2018, and it will grow another 8.4 percent in 2019 to total $421 billion (see Table 1). Organizations are expected to increase spending on enterprise application software in 2018, with more of the budget shifting to software as a service (SaaS). The growing availability of SaaS-based solutions is encouraging new adoption and spending across many subcategories, such as financial management systems (FMS), human capital management (HCM) and analytic applications.

Table 1. Worldwide IT Spending Forecast (Billions of U.S. Dollars)

|

| 2017 Spending | 2017 Growth (%) | 2018 Spending | 2018 Growth (%) | 2019 Spending | 2019 Growth (%) |

| Data Center Systems | 178 | 4.4 | 179 | 0.6 | 179 | -0.2 |

| Enterprise Software | 355 | 8.9 | 389 | 9.5 | 421 | 8.4 |

| Devices | 667 | 5.7 | 704 | 5.6 | 710 | 0.9 |

| IT Services | 933 | 4.3 | 985 | 5.5 | 1,030 | 4.6 |

| Communications Services | 1,393 | 1.3 | 1,427 | 2.4 | 1,443 | 1.1 |

| Overall IT | 3,527 | 3.8 | 3,683 | 4.5 | 3,784 | 2.7 |

Source: Gartner (January 2018)

The devices segment is expected to grow 5.6 percent in 2018. In 2017, the devices segment experienced growth for the first time in two years with an increase of 5.7 percent. End-user spending on mobile phones is expected to increase marginally as average selling prices continue to creep upward even as unit sales are forecast to be lower. PC growth is expected to be flat in 2018 even as continued Windows 10 migration is expected to drive positive growth in the business market in China, Latin America and Eastern Europe. The impact of the iPhone 8 and iPhone X was minimal in 2017, as expected. However, iOS shipments are expected to grow 9.1 percent in 2018.

"Looking at some of the key areas driving spending over the next few years, Gartner forecasts $2.9 trillion in new business value opportunities attributable to AI by 2021, as well as the ability to recover 6.2 billion hours of worker productivity," said Mr. Lovelock. "That business value is attributable to using AI to, for example, drive efficiency gains, create insights that personalize the customer experience, entice engagement and commerce, and aid in expanding revenue-generating opportunities as part of new business models driven by the insights from data."

"Capturing the potential business value will require spending, especially when seeking the more near-term cost savings. Spending on AI for customer experience and revenue generation will likely benefit from AI being a force multiplier — the cost to implement will be exceeded by the positive network effects and resulting increase in revenue," said Mr. Lovelock.

Gartner, Inc. forecasts worldwide enterprise security spending to total $96.3 billion in 2018, an increase of 8 percent from 2017. Organizations are spending more on security as a result of regulations, shifting buyer mindset, awareness of emerging threats and the evolution to a digital business strategy.

"Overall, a large portion of security spending is driven by an organization's reaction toward security breaches as more high profile cyberattacks and data breaches affect organizations worldwide," said Ruggero Contu, research director at Gartner. "Cyberattacks such as WannaCry and NotPetya, and most recently the Equifax breach, have a direct effect on security spend, because these types of attacks last up to three years."

This is validated by Gartner's 2016 security buying behavior survey*. Of the 53 percent of organizations that cited security risks as the No. 1 driver for overall security spending, the highest percentage of respondents said that a security breach is the main security risk influencing their security spending.

As a result, security testing, IT outsourcing and security information and event management (SIEM) will be among the fastest-growing security subsegments driving growth in the infrastructure protection and security services segments (see Table 1).

Table 1

Worldwide Security Spending by Segment, 2016-2018 (Millions of Current Dollars)

|

| 2016 | 2017 | 2018 |

| Identity Access Management | 3,911 | 4,279 | 4,695 |

| Infrastructure Protection | 15,156 | 16,217 | 17,467 |

| Network Security Equipment | 9,789 | 10,934 | 11,669 |

| Security Services | 48,796 | 53,065 | 57,719 |

| Consumer Security Software | 4,573 | 4,637 | 4,746 |

| Total | 82,225 | 89,133 | 96,296 |

Source: Gartner (December 2017)

Gartner analysts said that several other factors are also fuelling higher security spending.

Regulatory compliance and data privacy have been stimulating spending on security during the past three years, in the US (with regulations such as the Health Insurance Portability and Accountability Act, National Institute of Standards and Technology, and Overseas Citizenship of India) but most recently in Europe around the General Data Protection Regulation coming into force on 28th May 2018, as well as in China with the Cybersecurity Law that came into effect in June 2016. These regulations translate into increased spending, particularly in data security tools, privileged access management and SIEM.

Gartner forecasts that by 2020, more than 60 percent of organizations will invest in multiple data security tools such as data loss prevention, encryption and data-centric audit and protections tools, up from approximately 35 percent today.

Skills shortages, technical complexity and the threat landscape will continue to drive the move to automation and outsourcing. "Skill sets are scarce and therefore remain at a premium, leading organizations to seek external help from security consultants, managed security service providers and outsourcers," said Mr. Contu. "In 2018, spending on security outsourcing services will total $18.5 billion, an 11 percent increase from 2017. The IT outsourcing segment is the second-largest security spending segment after consulting."

Gartner predicts that by 2019, total enterprise spending on security outsourcing services will be 75 percent of the spending on security software and hardware products, up from 63 percent in 2016.

Enterprise security budgets are also shifting towards detection and response, and this trend will drive security market growth during the next five years. "This increased focus on detection and response to security incidents has enabled technologies such as endpoint detection and response, and user entity and behavior analytics to disrupt traditional markets such as endpoint protection platforms and SIEM," said Mr. Contu.

2020 will be a pivotal year in AI-related employment dynamics, according to Gartner, Inc., as artificial intelligence (AI) will become a positive job motivator.

The number of jobs affected by AI will vary by industry; through 2019, healthcare, the public sector and education will see continuously growing job demand while manufacturing will be hit the hardest. Starting in 2020, AI-related job creation will cross into positive territory, reaching two million net-new jobs in 2025.

"Many significant innovations in the past have been associated with a transition period of temporary job loss, followed by recovery, then business transformation and AI will likely follow this route," said Svetlana Sicular, research vice president at Gartner. AI will improve the productivity of many jobs, eliminating millions of middle- and low-level positions, but also creating millions more new positions of highly skilled, management and even the entry-level and low-skilled variety.

"Unfortunately, most calamitous warnings of job losses confuse AI with automation — that overshadows the greatest AI benefit — AI augmentation — a combination of human and artificial intelligence, where both complement each other."

IT leaders should not only focus on the projected net increase of jobs. With each investment in AI-enabled technologies, they must take into consideration what jobs will be lost, what jobs will be created, and how it will transform how workers collaborate with others, make decisions and get work done.

"Now is the time to really impact your long-term AI direction," said Ms. Sicular. "For the greatest value, focus on augmenting people with AI. Enrich people's jobs, reimagine old tasks and create new industries. Transform your culture to make it rapidly adaptable to AI-related opportunities or threats."

Gartner identified additional predictions related to AI’s impact on the workplace:

AI has already been applied to highly repeatable tasks where large quantities of observations and decisions can be analyzed for patterns. However, applying AI to less-routine work that is more varied due to lower repeatability will soon start yielding superior benefits. AI applied to nonroutine work is more likely to assist humans than replace them as combinations of humans and machines will perform more effectively than either human experts or AI-driven machines working alone will.

By 2022, one in five workers engaged in mostly nonroutine tasks will rely on AI to do a job.

"Using AI to auto-generate a weekly status report or pick the top five emails in your inbox doesn't have the same wow factor as, say, curing a disease would, which is why these near-term, practical uses go unnoticed," said Craig Roth, research vice president at Gartner. "Companies are just beginning to seize the opportunity to improve nonroutine work through AI by applying it to general-purpose tools. Once knowledge workers incorporate AI into their work processes as a virtual secretary or intern, robo-employees will become a competitive necessity."

Leveraging technologies such as AI and robotics, retailers will use intelligent process automation to identify, optimize and automate labor-intensive and repetitive activities that are currently performed by humans, reducing labor costs through efficiency from headquarters to distribution centers and stores. Many retailers are already expanding technology use to improve the in-store check-out process.

Through 2022, multichannel retailer efforts to replace sales associates through AI will prove unsuccessful, although cashier and operational jobs will be disrupted.

However, research suggests that many consumers still prefer to interact with a knowledgeable sales associate when visiting a store, particularly in specialized areas such as home improvement, drugstores and cosmetics, where informed associates can make a significant impact on customer satisfaction. Though they will reduce labor used for check-out and other operational activities, retailers will find it difficult to eliminate traditional sales advisers.

"Retailers will be able to make labor savings by eliminating highly repetitive and transactional jobs, but will need to reinvest some of those savings into training associates who can enhance the customer experience," said Robert Hetu, research director at Gartner "As such most retailers will come to view AI as a way to augment customer experiences rather than just removing humans from every process."While many industries will receive growing business value from AI, manufacturing is one that will receive a massive share of the business value opportunity. Automation will lead to cost savings, while the removal of friction in value chains will increase revenue further, for example, in the optimization of supply chains and go-to-market activities.

In 2021, AI augmentation will generate $2.9 trillion in business value and recover 6.2 billion hours of worker productivity.

However, some industries, such as outsourcing, are seeing a fundamental change in their business models, whereby the cost reduction from AI and the resulting productivity improvement must be reinvested to allow reinvention and the perusal of new business model opportunities.

"AI can take on repetitive and mundane tasks, freeing up humans for other activities, but the symbiosis of humans with AI will be more nuanced and will require reinvestment and reinvention instead of simply automating existing practices," said Mike Rollings, research vice president at Gartner. "Rather than have a machine replicating the steps that a human performs to reach a particular judgment, the entire decision process can be refactored to use the relative strengths and weaknesses of both machine and human to maximize value generation and redistribute decision making to increase agility."

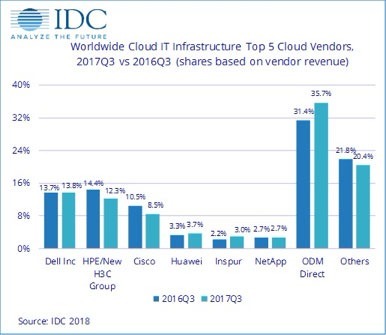

According to the International Data Corporation (IDC) Worldwide Quarterly Cloud IT Infrastructure Tracker, vendor revenue from sales of infrastructure products (server, storage, and Ethernet switch) for cloud IT, including public and private cloud, grew 25.5% year over year in the third quarter of 2017 (3Q17), reaching $11.3 billion.

Public cloud infrastructure revenue grew 32.3% year over year in 3Q17 to $7.7 billion and now represents 30.2% of total worldwide IT infrastructure spending, up from 26.3% one year ago. Private cloud revenue reached $3.6 billion for an annual increase of 13.1%. Total worldwide cloud IT infrastructure revenue is on pace to nearly double in 2017 when compared to 2013. Traditional (non-cloud) IT infrastructure revenue grew 8.0% from a year ago, although it has been generally declining over the past several years; despite the declining trend, at $14.2 billion in 3Q17 traditional IT still represents 55.6% of total worldwide IT infrastructure spending.

Public cloud also represented 68.0% of the total cloud IT infrastructure revenue in 3Q17. The market with the highest growth in the public cloud infrastructure segment was Storage Platforms with revenue up 45.1% compared to the same quarter of the previous year, and making up 42.0% of the revenue in public cloud. Compute Platforms and Ethernet Switch public cloud IT infrastructure revenues were up 24.8% and 23.2%, respectively. Compute Platforms represented 43.9% of public cloud IT infrastructure revenue. Private cloud infrastructure revenue was driven by the Storage Platforms growth of 16.1% year over year.

"2017 has been a strong year for public cloud IT infrastructure growth, accelerating throughout the year," said Kuba Stolarski, research director for Computing P latforms at IDC. "While hyperscalers such as Amazon and Google are driving the lion's share of the growth, IDC is seeing strong growth in the lower tiers of public cloud and continued growth in private cloud on a worldwide scale. In the near term, new Intel and AMD platforms released during 2017 should aid in refresh and infrastructure expansion throughout the cloud IT infrastructure segment."

Except for Latin America revenue, which grew 5.0% from a year ago, all other regions in the world grew their cloud IT Infrastructure revenue by double digits. Asia/Pacific (excluding Japan) and Central and Eastern Europe (CEE) saw the fastest growth rates at 50.1% and 35.3%, respectively. Canada (22.5%) and Western Europe (24.6%) had annual growth in the twenties, while the U.S. (18.7%), Japan (17.5%), and Middle East & Africa (MEA) (15.8%) had annual growth in the teens.

| Top Companies, Worldwide Cloud IT Infrastructure Vendor Revenue, Market Share, and Year-Over-Year Growth, Q3 2017 (Revenues are in Millions) | |||||

| Company | 3Q17 Revenue (US$M) | 3Q17 Market Share | 3Q16 Revenue (US$M) | 3Q16 Market Share | 3Q17/3Q16 Revenue Growth |

| 1. Dell Inc | $1,557 | 13.8% | $1,237 | 13.7% | 25.9% |

| 2. HPE/New H3C Group** | $1,388 | 12.3% | $1,299 | 14.4% | 6.9% |

| 3. Cisco | $958 | 8.5% | $943 | 10.5% | 1.6% |

| 4. Huawei* | $419 | 3.7% | $300 | 3.3% | 39.5% |

| 4. Inspur* | $344 | 3.0% | $202 | 2.2% | 70.7% |

| 4. NetApp* | $307 | 2.7% | $240 | 2.7% | 28.0% |

| ODM Direct | $4,043 | 35.7% | $2,831 | 31.4% | 42.8% |

| Others | $2,306 | 20.4% | $1,970 | 21.8% | 17.0% |

| Total | $11,322 | 100.0% | $9,022 | 100.0% | 25.5% |

| IDC's Quarterly Cloud IT Infrastructure Tracker, Q3 2017 January 11, 2018 | |||||

Notes:

* IDC declares a statistical tie in the worldwide cloud IT infrastructure market when there is a difference of one percent or less in the vendor revenue shares among two or more vendors.

** Due to the existing joint venture between HPE and the New H3C Group, IDC will be reporting external market share on a global level for HPE as "HPE/New H3C Group" starting from Q2 2016 and going forward.

Research shows that managed services may be the only chance for growth in the IT industry’s channel; resellers are still switching to this sales model in large numbers, but the sales process and customers relationships are very different; and some of the technology issues need new skills.

Managed services in 2018 will need to deal with a number of issues – some, like security are external, others like the changes needed in sales processes and customer engagement and security, are internal factors. One the main pressures will continue to be the availability of skilled resources, both in sales and in the area of security, where GDPR, to be introduced in May 2018, will provide the main impetus for re-analysis of their positions by most MSPs.

Research from IT Europa ( http://www.iteuropa.com/?q=market-intelligence/managed-service-providers-europe-msps-top-1000) and others shows that there is a continuing race to scale as the economics of managed services depend on having a large customer base, but at the same time, because of the expertise needed to deliver specific vertical market applications, many are having to build on their strengths and specialist further.

The changing nature of managed services….

The bigger MSPs are growing fastest, says the research, and in Europe, the Netherlands has overtaken Germany in numbers of large MSPs. The Netherlands has seen a dramatic acceleration in the number of data centres situated there in recent years. The UK is still biggest, and now has 36% of Europe’s largest managed services providers and is the largest individual market. The technology is changing as well: when asked about what is on the horizon, MSPs say Internet of Things (IoT) has started to appear as an MSP solution area.

This latest study of Europe’s managed services providers shows increased consolidation as well as more specialisation by application area. In the study of the top 1500 MSPs 2017, the listed companies – 112 in number - saw their sales rise by 7.5% yr/yr. The smaller independents by contrast managed a lower 5.5% growth. One reason for the changes has been the rush for scale among managed services companies, with a high rate of mergers among the small players, and acquisitions by larger firms. There seems to be no shortage of available funding, either from the industry itself or venture capital.

These results and a wider discussion on the changing nature of the MSP will be a feature of the

Managed Services & Hosting Summit – Europe, at the Novotel Amsterdam City • Amsterdam on 29th May 2018 (http://www.mshsummit.com/amsterdam/index.php).

This is an invitation-only executive-level conference exploring the business opportunities for the ICT channel around the delivery of Managed Services and Hosting. Topics for discussion will include sales and marketing processes, GDPR, building value in a business with an eye on the mergers and acquisitions market, and skills development to get into those higher margin areas. This is a timely event as the rapid and accelerating change in the way customers wish to purchase, consume and pay for their IT solutions is forcing the channel to completely redefine its role, business models and relationships.

The Managed Services & Hosting Summit is firmly established as the leading managed services event for channel organisations. Now in its eighth year as a UK event, the Managed Services & Hosting Summit Europe is being staged for the second time in Amsterdam and will examine the issues facing Managed Service Providers, hosting companies, channel partners and suppliers as they seek to add value and evolve new business models and relationships.

The Managed Services & Hosting Summit – Europe 2018 features conference session presentations by major industry speakers and a range of breakout sessions exploring in further detail some of the major issues impacting the development of managed services.

The summit will also provide extensive networking time for delegates to meet with potential business partners. The unique mix of high-level presentations plus the ability to meet, discuss and debate the related business issues with sponsors and peers across the industry, makes this a must attend event for any senior decision maker in the ICT channel.

The next Data Centre Transformation events, organised by Angel Business Communications in association with DataCentre Solutions, the Data Centre Alliance, The University of Leeds and RISE SICS North, take place on 3 July 2018 at the University of Manchester and 5 July 2018 at the University of Surrey.

For the 2018 events, we’re taking our title literally, so the focus is on each of the three strands of our title: DATA, CENTRE and TRANSFORMATION.

The DATA strand will feature two Workshops on Digital Business and Digital Skills together with a Keynote on Security. Digital transformation is the driving force in the business world right now, and the impact that this is having on the IT function and, crucially, the data centre infrastructure of organisations is something that is, perhaps, not as yet fully understood. No doubt this is in part due to the lack of digital skills available in the workplace right now – a problem which, unless addressed, urgently, will only continue to grow. As for security, hardly a day goes by without news headlines focusing on the latest, high profile data breach at some public or private organisation. Digital business offers many benefits, but it also introduces further potential security issues that need to be addressed. The Digital Business, Digital Skills and Security sessions at DTC will discuss the many issues that need to be addressed, and, hopefully, come up with some helpful solutions.

The CENTRES track features two Workshops on Energy and Hybrid DC with a Keynote on Connectivity. Energy supply and cost remains a major part of the data centre management piece, and this track will look at the technology innovations that are impacting on the supply and use of energy within the data centre. Fewer and fewer organisations have a pure-play in-house data centre real estate; most now make use of some kind of colo and/or managed services offerings. Further, the idea of one or a handful of centralised data centres is now being challenged by the emergence of edge computing. So, in-house and third party data centre facilities, combined with a mixture of centralised, regional and very local sites, makes for a very new and challenging data centre landscape. As for connectivity – feeds and speeds remain critical for many business applications, and it’s good to know what’s around the corner in this fast moving world of networks, telecoms and the like.

The TRANSFORMATION strand features Workshops on Automation and The Connected World together with a Keynote on Automation (Ai/IoT). IoT, AI, ML, RPA – automation in all its various guises is becoming an increasingly important part of the digital business world. In terms of the data centre, the challenges are twofold. How can these automation technologies best be used to improve the design, day to day running, overall management and maintenance of data centre facilities? And how will data centres need to evolve to cope with the increasingly large volumes of applications, data and new-style IT equipment that provide the foundations for this real-time, automated world? Flexibility, agility, security, reliability, resilience, speeds and feeds – they’ve never been so important!

Delegates select two 70 minute workshops to attend and take part in an interactive discussion led by an Industry Chair and featuring panellists - specialists and protagonists - in the subject. The workshops will ensure that delegates not only earn valuable CPD accreditation points but also have an open forum to speak with their peers, academics and leading vendors and suppliers.

There is also a Technical track where our Sponsors will present 15 minute technical sessions on a range of subjects. Keynote presentations in each of the themes together with plenty of networking time to catch up with old friends and make new contacts make this a must-do day in the DC event calendar. Visit the website for more information on this dynamic academic and industry collaborative information exchange.

This expanded and innovative conference programme recognises that data centres do not exist in splendid isolation, but are the foundation of today’s dynamic, digital world. Agility, mobility, scalability, reliability and accessibility are the key drivers for the enterprise as it seeks to ensure the ultimate customer experience. Data centres have a vital role to play in ensuring that the applications and support organisations can connect to their customers seamlessly – wherever and whenever they are being accessed. And that’s why our 2018 Data Centre Transformation events, Manchester and Surrey, will focus on the constantly changing demands being made on the data centre in this new, digital age, concentrating on how the data centre is evolving to meet these challenges.

Couchbase helps revolutionise digital engagement for the fashion industry with Tommy Hilfiger.

In the global fashion industry, digital innovation plays a critical role in keeping in step with the needs of both consumers and customers. In the era of instant gratification, brands need to deliver a “wow” factor through engaging experiences, which keep them at the forefront of not only consumers’ minds, but also those of retail and wholesale partners. Staying competitive can mean offering consumers new ways to shop or optimizing the sales process to reduce time to market for new collections. Tommy Hilfiger is one example of a global brand that is harnessing the potential of digital transformation to improve its partners’ experience.

The Challenge: Streamline sales and create a more attractive experience for retailers while maintaining sustainability and corporate responsibility.

As technology continues to revolutionize the way customers shop, success in the industry means keeping up with this at every single stage, from the showroom to the shop floor. As part of its digital strategy, Tommy Hilfiger aims to streamline its sales processes and shorten the window between retailer previews of new collections and actually delivering those new products to stores. At the same time, the company seeks to minimize the need to produce and transport samples: reducing costs while maintaining the company’s ongoing drive towards sustainability and corporate responsibility by minimizing the environmental impact that comes with sample creation and shipping throughout the supply chain.

Couchbase’s data platform has supported Tommy Hilfiger in realizing this ambition with the introduction of global Digital Showrooms. By allowing buyers to browse collections, view pieces, and create custom laydowns and orders via touchscreen workstations and a theatre of ultra-high-definition, 4K screens, the Digital Showroom offers a forward-thinking approach to the sales process. It removes the need to create, examine, and deliver samples to retail locations around the world for every new collection. As a result, Tommy Hilfiger can deliver a transformational, engaging experience to partners as they browse and buy the season’s new collection.

Couchbase recognized that in order for the Digital Showroom to provide a truly tailored experience for retail and wholesale partners, it needed a data platform to support this new approach to sales: delivering an easy-to-use, reliable experience to partners.

• Access and share product specifications in real time according to each customer’s needs

• Support a one-click ordering system to complete sales and deliver products onto store shelves faster

• Add new product lines and functionalities as they are created

• Support in-depth analysis of customer orders to help develop a more targeted, relevant, and successful sales experience

• Allow the Digital Showroom to be easily replicated in various locations around the world

The Solution: Couchbase underpins the Digital Showroom with the most powerful NoSQL platform.

Couchbase provided the ideal data platform to underpin the Digital Showroom and help build an engaging digital experience that had never existed before. As the most powerful NoSQL platform available, Couchbase has the flexibility, scalability, and power to support the Digital Showroom’s needs and ambition. Couchbase’s ease of use also meant that the technology rollout was very straightforward.

The Result: A scalable, digitally engaging buying experience and faster time to market for new collections.

Faster sales, greater sustainability Couchbase’s technology has contributed to the success of the Digital Showroom since its launch in 2015. The expected benefits of a faster sales process and reduced sample production are already being realized. For instance, when Tommy Hilfiger’s Asia-Pacific team visited Europe for a buying session, the visit was significantly shortened from the usual three days to just one. It is also recording sales increases, with pre-Fall sales for the Middle East, Africa, and the Netherlands already growing.

Anywhere, anytime engagement With Couchbase, Tommy Hilfiger can develop and deliver a universally engaging experience regardless of device, location, or connectivity. The company can add, access, and combine data in real time due to Couchbase’s NoSQL architecture, so retailers can not only inspect, modify, and create orders as they browse collections, but also place their final order and arrange delivery immediately. At the same time, the Couchbase data platform can reliably operate offline without depending on constant network access to a central data store.

Scaling and expanding to keep pace with growth The Couchbase data platform scales quickly and easily, supporting growth and expansion of the Digital Showroom as well as other innovation initiatives that help the company improve business processes. Tommy Hilfiger can also continuously add to the number of collections available through the Digital Showroom and expand the concept to locations across the world. From the first launched in Amsterdam, there are now 24 Digital Showroom theatres with 59 workstations, in nine cities across the globe: Amsterdam, Milan, Paris, London, Dusseldorf, Stockholm, Copenhagen, New York, and Hong Kong.

With an ambitious rollout plan by the end of 2018, the aim is to have Digital Showrooms in more than 25 locations worldwide with over 100 workstations. With Couchbase powering the Digital Showroom, Tommy Hilfiger can offer a consistently engaging, integrated, and seamless brand buying experience across every market and showroom regardless of market or customer size, anywhere in the world.

“Our Digital Showroom revolutionizes the buying and selling journey for our retail customers and internal sales teams,” said Daniel Grieder, CEO, Tommy Hilfiger. “We are passionate about providing our clients with the best service, experience, and quality. Our Digital Showroom concept completely reimagines the traditional buying approach and establishes a new fashion industry benchmark for business-to-business sales. The concept also supports our ongoing focus on efficiency and will significantly streamline and enhance the Tommy Hilfiger sales experience.”

Wayne Carter, chief architect of mobile at Couchbase said: “Ultimately, the future of retail is digital. It’s no exaggeration to say that Tommy Hilfiger and its Digital Showroom are changing the fashion industry forever and its success is a model for all other brands to follow. Ten years ago, this kind of project would have been unimaginable, with the digital experience sorely lacking. Today, however, digital is as good as real; and often better. In time, both consumers and retailers will expect the digital experience and in-person experience to overlap seamlessly. The ability to access data, and use it to engage with these audiences, will be critical to ensuring success.”

Boosts service quality while reducing costs compared to previous operating system.

In the global cloud hosting arena, City Network stands out from the pack thanks to superb service quality and a unique focus on industry-specific regulatory compliance. Always on the lookout for new ways to enhance this competitive edge, City Network realized Ubuntu offered a highly compelling alternative to its existing, legacy Linux operating system. Easier to use, easier to manage, and backed by Canonical’s expert support, Ubuntu is helping City Network reach new heights of quality and customer satisfaction.

Marrying compliance, transparency, and agility

Today, agility is the key to business success. Companies in every industry are striving to deliver new services more quickly, and they are constantly looking for ways to increase the pace and cost-effectiveness of innovation.

This trend has led to a significant rise in the popularity of infrastructure-as-a-service (IaaS). One of the primary elements of any digital transformation, cloud hosting can deliver the scalability, performance, and flexibility to dramatically improve time-tomarket on new products and services. Yet, for many businesses, stringent laws and regulations make it difficult to adopt IaaS while remaining compliant. This is a problem in particular for highly regulated sectors such as financial services, but with the EU general Data Protection Regulation looming, compliance is becoming an increasingly widespread concern.

This is where City Network comes in – bridging the gap between agility and compliance.

Johan Christenson, CEO of City Network, explains: “The IaaS market is dominated by giants, yet those giants largely ignore the compliance niche. In addition to our flagship public cloud, we also offer semi-private, private, and hybrid ‘Compliant Cloud’ services. These services are tailored to satisfy a vast number of international ISO standards and industry-specific regulations, so our customers can enjoy the advantages of cloud hosting without having to worry about compliance.”

For City Network, quality is everything, so it is always alert to new ways that it can improve its services and sharpen its competitive edge. As a strong proponent of openness and transparency, in 2014 City Network became the first European hosting provider to offer OpenStack to its customers and today, City Network runs the most OpenStack-based public cloud nodes in the world. Yet recently, the company decided that its existing operating system was not providing the best platform for its OpenStack services.

“We knew that there was room to improve when it came to our underlying operating system,” continues Johan Christenson. “It’s important to us to be as nimble as possible, yet the Linux distribution we were using could be unwieldy and it lacked responsive support. What’s more, it wasn’t especially cost-effective. It was clear that the time had come to find a new solution.”

New platform, new partner

City Network set its sights on finding an alternative operating system that was easier to manage, more reasonably priced, and better supported and Ubuntu emerged as the ideal solution.

“We chose Ubuntu for several reasons,” explains Johan Christenson. “The first is quality: the processes that Canonical has put in place made us confident that Ubuntu is the best option for supporting OpenStack on a global scale.

“Second is ease-of-use. Ubuntu is highly intuitive, so our devs can work quickly and accurately and simplicity brings quality. Additionally, the flexibility of how Canonical delivers OpenStack makes it much easier to implement compliance in a scalable way.

“Canonical’s support were also more responsive to our needs, and they were keen to work with us to address our specific challenges.

“Ultimately, we found that Ubuntu was less expensive and more effective than our existing operating system gradually switching to Ubuntu was a unanimous, corporation-wide decision.”

Once City Network received the go-ahead from its regulatory team, the company immediately went ahead with its plan to make Ubuntu its platform of choice, beginning the process of implementing the operating system at all of its 20 data centres worldwide.

to manage its Ubuntu deployments and streamline new cloud launches, City Network is utilising the tools and support delivered by Canonical through the Ubuntu Advantage package. As an Ubuntu Certified Public Cloud Partner, City Network has the further benefit of regularly updated, certified Ubuntu cloud images, which guarantee optimal performance.

Partnering with Canonical also gives City Network the option to sell Ubuntu Advantage on to its own users. This opens up additional revenue streams for City Network, and enables its customers to enjoy direct support from Canonical.

Johan Christenson comments: “Banks and insurance companies demand a very high level of security and support. So being able to offer Ubuntu Advantage is critical for us.”

Despite the challenges involved in migrating such a large production environment to a new platform, the process is going as smoothly as can be expected, and City Network is on track to complete the move by the end of the year.

Quality, flexibility, value

So far, City Network has transitioned seven data centres over to Openstack on Ubuntu, and it is already seeing considerable benefits.

“Few companies run OpenStack operationally on the scale that we do,” says Johan Christenson. “Being able to run so many connected data centres is massive. With Ubuntu we can keep the quality up and upgrade without downtime it works really well.”

Since Ubuntu is so much easier to work with, City Network’s employees are significantly happier. The company’s operating costs are also lower, and it is able to pass on these saving to its users.

Most importantly, Ubuntu is leading to happier customers, as Johan Christenson explains: “We’re coming in with a package that customers really appreciate. We’re delivering high quality at a fair price, and our clients trust in our services not just in City Network itself, but in the operating system and support as well.”

Switching to Ubuntu positions City Network perfectly to support digital transformation in the financial services sector. As the drive towards agility grows, financial institutions are becoming increasingly interested in using Ubuntu as their core operating system.

“Recently, one of Sweden’s leading banks engaged us to host the infrastructure for the heart of their business,” confirms Johan Christenson. “This is the first time City Network will be hosting the mission-critical applications of such a large bank, and Ubuntu was essential in securing the deal. Like us, Canonical are nimble and fairly priced – so together we can provide the flexibility that the bank requires, combined with compliance and value.”

Johan Christensen concludes: “Ubuntu is an ideal fit, both functionally and philosophically. From our perspective, there’s no better operating system for OpenStack.”

Since the earliest ecommerce sites went live online, journalists, retail pundits and internet commentators have spoken about the so-called “death of the high street”. But with two decades having passed since those early days of the internet, the vast majority of retailers are still yet to see a complete transition to online shopping.

By Geoff Galat, CMO at Clicktale.

While ecommerce may not yet have forced all traditional retailers out of business, there is no denying that the high street is in a sharp period of decline. According to the latest ONS retail statistics, high street shopping is at a near all-time low, with online sales rising by 21% in the last four years. Seeing this decline, retail commentators predict that half of the UK’s shop premises will have disappeared by 2030, forcing ever more retailers – and customers – online.

Faced with this migration into the digital space, retailers must begin to look for ways to provide their customers with the same standards of experience that they have come to expect in more traditional high street stores.

Simply focusing on converting browsers into customers is no-longer enough. Businesses must now look to understand their customers’ digital experiences – tailoring their approach to individual mindsets, personas and buying moods. The “success” of an online store cannot be measured by mere conversion rates alone, it must be defined by customer experiences, incorporating insights from consumer behaviours, shopping trends and long-term browsing habits.

So how can brands meet this demand and get on board with the digital shift in order to create better customer experiences? Here are five ways that businesses can get started:

To understand and interpret customer needs, brands must reflect on information received from their ‘digital body language’. In our day to day lives we obtain information from others around us; non-verbal clues, facial expressions and gestures. In a traditional high street store, this body language can be vital in deciding how and when to approach a customer or to tailor their experience for the best possible results. In an online environment however, the inability to read a customer’s body language can make it extremely difficult for retailers to tailor their experiences.

This is where digital body language comes in. Through the use of Experience Analytics retailers can anonymously analyse subconscious online behaviours such as micro-signals and gestures – helping to gain an understanding of the customers’ happiness or displeasure, then adapting accordingly.

This layer of insight is advantageous when creating tailor-made digital experiences for customers visiting the retailer’s online store. Instead of being given a one-size-fits-all interaction, they will have an experience better suited to their personal needs, with the path to purchase becoming more linear and ultimately providing a better business outcome.

Regardless of the data available to them, retailers cannot change the mind-sets of the customers arriving on their websites. What they can do however, is use their insights to create a better environment around these customers.

By analysing a customer’s digital body language, retailers can begin to bridge the gap between customer expectations and the realities of online shopping. Taking on the role of a salesperson on the shop floor, such insights can be used to aid a confused customer, resolving potential issues instantly and preventing them from happening again. Each time a problem is resolved, there is potential for the customer journey to improve – a rewarding outcome for both customers and brands.

Online retailers must learn to accept that every customer is unique, with personality traits, moods and different ways of browsing online environments. The process of understanding digital body language must be carefully achieved over a period of time, as each customer provides something original and valuable. By tracking visitor patterns and clicks, and using visualisation tools such as heat-maps, brands can uncover a wealth of rich ‘body language’ data that traditional analytics would never uncover.

For many retailers, digital body language remains a new and largely unexplored concept. In reality however, it is only the tip of a much larger trend – the shift towards big data and Experience Analytics.

Once a retailer has developed enough data about the digital body language of its customers, it can begin to cross examine that data, finding patterns and trends across the brand’s entire customer base. As these insights develop, customer archetypes can be narrowed down and filtered into detailed categories which can become increasingly refined over time. These in-depth insights can prove crucial for understanding the different states of minds that customers experience when they shop.

Over time it will become clear how important it is to understand digital body language and have customer experience embedded at the very heart of online retail brands. The ability to construct an extensive database of customer knowledge gives retailers scope to build rapport with customers, allowing both parties to ultimately benefit from this improved relationship.

Retail is evolving at a faster pace than any time in recent memory, with mobile firmly established as the platform of the future. Retailers that are still merely ‘cobbling’ platforms together risk being left behind as customers want a quick and seamless omni-channel experience and will go elsewhere if brands cannot provide this.

By Scott Clarke, Chief Digital Officer and Global Consulting Leader for Retail, Consumer Goods, Travel and Hospitality, Cognizant.

So what is the key to maintaining a competitive edge? Simply put, it is technology: the catalyst for getting consumers into stores, the brains behind every interaction, and shaping every angle of the customer experience. As omni-channel blurs the line between online and offline, retailers should make it their mission to improve the customer’s shopping experience on both. Here, we discuss the five biggest trends set to boost the customer experience and brand loyalty in retail over the coming year.

1. Conversational AI

By 2020, more than two billion people will use conversational AI on a regular basis. It will become a vital – and possibly the primary – tool for finding, researching and buying products.

In a conversational AI world, virtual assistants will search, open, fetch, command and engage the dozen or more websites, portals, apps and systems we all interact with on a daily basis. “My virtual agent does that” will become the new “there is an app for that”. And whether businesses sell value meals, luxury clothes, airline tickets, sports cars or hotel rooms, there are two important considerations to make a success of the voice-enabled marketplace. Firstly, retailers must make it easy for their customers to find them when they are simply using their voice. Secondly, they must make the buying process seamless once consumers connect to the brand. While some retailers have already made headway, others need to update their strategies to make sure they are prepared for this voice enabled reality.

2. Ultra-fast delivery

Speed and convenience have been key drivers in the retail sector for years. Research shows that 72 percent of consumers would spend more if they could be sure of same-day delivery, while figures indicate the UK high street missed out on almost £5 billion in sales mainly due to not having a same-day delivery option. But distribution is about to be super-charged, with Amazon already talking about 30-minute drone delivery as the capabilities of drones improve day-by-day.

Advancements in autonomous piloting, ‘sense and aware’ technologies and increased battery life mean that delivery drones show promise to be the next disruptive technology within the retail supply chain. In fact, the market is projected to reach $5.59 billion by 2020. Businesses would do well to start investigating strategies now to see if they would fit their business model. Whether to speed up retail deliveries or bring key parts and equipment to heavy industry projects, drones have the potential to enhance process efficiency and reduce costs.

3. Providing richer customer experiences

As technology drives greater innovation and access to new products, the differentiator becomes all about the customer’s experience with the brand. We anticipate more and more retailers will increase their focus on creating omni-channel shopping experiences that are highly personalised, contextual and compelling. The focus will be on delighting customers at each point of interaction, regardless of channel.

With more shoppers engaging in an omni-channel process before purchasing, it will become increasingly important to integrate physical and digital retail experiences. Utilising new technologies such as virtual agents, mobile wallet payments, beacons, face and object recognition, magic mirrors, and smart shelves, will help provide richer customer experiences, drive more footfall to physical stores and increase sales conversions.

4. Robotic tailoring

Personalisation is the battleground for various industries, including retail. However, in many cases, too much choice has diminished the experience of the customer, not enhanced it. We all feel this from time-to-time: too many different brands, colours, shapes and materials to choose from can actually be off-putting and stop us from shopping altogether.

In the future, retailers will produce bespoke and tailored clothing items in a matter of hours, rather than days or weeks. Consumers will no longer go into a store and buy a small or medium sized jumper. 3D body imaging in-store will allow retailers to retain customers’ measurements and preferences, enabling them to create tailored clothing, quickly en masse.

5. Smart stores

Admittedly, many brands have ploughed money into integrating technology into their physical stores to compete for footfall. However, it may not have taken off as expected, because many went head first into the investment without ensuring the appropriate back-end infrastructure, or training for sales assistants was in place to make the most of the benefits that in-store technology can bring. There is simply no point in retailers spending huge amounts of money on in-store technology if it does not work properly and nobody knows how to use it.

However, when done well smart stores have the ability to boost the bottom line. High-end retailer, Rebecca Minkoff, saw sales shoot up by more than 200 percent following the introduction of interactive touch-screens that let shoppers choose products to be sent to their dressing rooms. These dressing rooms also include interactive mirrors that can adjust lighting and contact sales associates. Screens will allow people to view the clothes they are trying on in different colours, sizes and looks, completely personalising the customer experience.

Start preparing now, the future is not that far away

If this decade thus far has taught us anything, it is that technological disruption is unpredictable. Mobile shopping may be the driving force in retail today, but in another decade, virtual and augmented reality could be shaping consumer trends. In retail, as in fashion, no one size will fit all, so retailers must use the data that they have at their fingertips to tailor their services to every individual customer’s preferences.

Our recent survey – The Digital Transformation PACT – found that many organizations are starting to leverage new technology which will radically change the way they do business. We tend to think of these organisations as financial institutions experimenting with blockchain, or manufacturers utilising IoT. What we don’t often think of is how digital is transforming traditional industries like agriculture.

By James Maynard, Offering Management Director – Innovative IoT Business Unit at Fujitsu.

Our survey found that 86% of businesses leaders believe that the ability to change will be crucial to their business’ survival in the next five years. As such the pairing of technology with farming and agriculture is what will shape and drive the agricultural industry in the years to come.

The forces driving this shift are, in many ways, bigger even than technology. The Food and Agriculture Organization of the United Nations predicted in 2009 that globally we need to produce 70% more food for an additional 2.3 billion people by 2050. The socio-economic pressures of this type of demand on our resources ae huge, and in this case technology can act as an enabler for solutions to what is a very serious and complex problem.

To cope with demand, and drive efficiency in the production process, farmers are increasingly turning to using more advanced technology than just five years ago. At Fujitsu we’ve been experimenting with human-centric IoT initiatives like our UBIQUITOUSWARE solutions, what we didn’t expect to be able to develop is something for livestock. Building a ‘Connected Cow’ to support livestock farmers.

The Connected Cow is a system whereby a pedometer monitors the steps a cow takes in a 24-hour period. It sends this data to the cloud, analyses it, and then accurately identify when oestrus – the period of fertility – starts. This data goes to the farmer’s smartphone, tablet or PC, and lets them know when they can artificially inseminate the cow in the optimal time frame.

With this Connected Cow technology the success rate of artificially inseminating cows rises from 44% to 90%. It has been shown that improving the detection of oestrus in dairy cows by 10% above the national average can improve profitability by 0.97p /litre.

It is an example of how the Internet of Things (IoT) as a whole is less about the individual components that collect the data, and more about the systems that can solve problems or industrial challenges in a practical way.

With increasing demand for more advanced technology, it comes as no surprise that a recent survey by McDonald's of UK farmers found that tech talent is becoming crucial for the farming industry.

Speaking to farmers across the country, 61% said they believe technology will have an impact on their business over the next five years.

Three quarters said they would need more access to digital and technology skills and more than half to data and coding knowledge. A further 81% went on to say that access to the right skills is their top priority over the coming 12 months.

In an industry that every individual in the world relies upon, farmers simply cannot afford to stand still - so it’s encouraging to see British farmers are being front-footed in their investment in technology and skills.

Our Digital Transformation PACT survey looked at the ingredients businesses need to successfully digitally transform, and found that businesses must focus on four strategic elements: People, Actions, Collaboration and Technology. It’s the people element that we’re seeing those in the framing industry struggling with most in being able to merge access to technology with the ability to apply it day-to-day.

Across the board, while organisations recognize the role of people in digital success and are taking steps to increase skills, there remains a problematic skills gap and businesses are conscious of the further impact of technological change.

As a technology provider we understand the need to support both industries in terms of solutions, but also the importance of working with educators to ensure there are enough people coming into the talent pool with the right skills to cope with the socio-economic pressures that industries like agriculture are facing.

Indeed schools are increasingly collaborating with industry partners to bring technology into the learning experience, and to provide learning that is practical and brings a sense of realism to subjects that can be difficult to comprehend.

At a time when British farming is facing a number of challenges, understanding how technology can be applied to empower farmers to achieve better results - while ensuring they have access to the right technology skills - is a vital step towards ensuring UK farming thrives.

The wearables market is one of the most talked about industries today, with its uses spanning far and wide across both consumers and businesses. Furthermore, it looks set to be a highly lucrative industry, with CCS Insights predicting it will be worth $20 billion by the year 2020.

By Dr. Shane Rooney, GSMA.

Although initially holding a reputation for being a ‘fun’ consumer-orientated market, wearables are now having a marked impact on a number of industries, proving to offer an enticing business opportunity. It seems consumers are also recognising the benefits, with the worldwide wearables market showing positive shipment growth at 10.3% year over year, reaching 26.3 million during the second quarter of 2017 alone, according to IDC.

While there are many examples of the growth of wearable technology across different sectors, healthcare is perhaps one industry that is seeing the greatest benefit, where devices are being used to track not only general fitness, but the well-being and safety of people across the globe.

Connected wearable devices, such as wristbands and heart monitors also offer benefits to the elderly, increasing access to health information and driving healthcare efficiencies. Heart monitors, for example can help to monitor vital signs, such as temperature and heart rate but they are also proving indispensable when it comes to signalling when elderly people suffer a fall. If the wearer of a connected device falls, the device can automatically alert friends and relatives, reducing the length of time they spend on the floor and the likelihood that they will need to be admitted to hospital.

Why mobile matters

Connected wristbands need to be fully mobile, rather than relying on a nearby hub or phone to communicate data. A fully mobile device can track the wearer’s location and status both inside and outside the home. To minimise the need to replace or recharge batteries, wearable devices also need to be very power-efficient. Employing low power wide area (LPWA) connectivity could increase a wearable’s battery life fivefold in comparison to conventional 2G cellular connectivity, according to Machina Research[1], meaning they work in a better and safer way, for whoever is using them.

LPWA networks are an emerging, high-growth area of the Internet of Things that complement and extend conventional wide area networks that make use of 2G, 3G and 4G cellular technologies. These types of networks are designed for low cost applications that have low data rates, long battery lives, long reach and operate in remote and hard to reach locations where existing mobile technologies are unable to penetrate.

Some of these gains could be used to streamline the form factor of the wearable device, as well as to increase the frequency of transmitted sensor readings, improving the related analytics. If they are equipped with a voice-capable LPWA technology, such as LTE-M, wearables can also support mobile voice communications to make emergency calls.

An example of this is happening right now in Denmark, where TDC Group is piloting a wristwatch that can monitor the wearer’s vital signs, providing live healthcare data to clinics and hospitals. TDC’s joint venture with Leikr and a local start-up MedHub is supplying the watches for the healthcare pilot using NB-IoT technology.

Just as the technology within the wearable device itself continues to evolve, it is clear so too will the way in which wearables are used, to meet ever changing needs and use cases. However, what will not change, is the need for these connected devices to be mobile, always connected and fully operational - even more so as they move further into the healthcare and assisted living space, where real time updates are fundamental. The unique attributes of NB-IoT technology, and LPWA networks means this type of connected infrastructure has the potential to support a number of wearable technology use cases – allowing innovators and operators to ensure successful deployment of new devices as the IoT industry takes holds.

Jason Kay, CCO, IMS Evolve, explains the role digitisation is playing in transforming the cold food chain to eradicate waste, improve food safety and mitigate the risk of a global food crisis.

The world today has a vast problem with food – from a lack of biodiversity to excessive wastage, from poor health linked to over consumption to massive food poverty. We grow enough food to feed 12 billion – far in excess of the seven billion population – yet more than one billion people are under fed. The UN estimates that, on our current path of food consumption and waste, by 2050 we will reach a tipping point and the world will be in a food crisis.

The problems extend from agriculture all the way through the food supply chain to the home, where food wastage – in more economically developed countries at least – is excessive. The UN target calls for the world to cut per capita food waste in half by 2030 – but while changing consumer education and expectation is essential, as is the drive to increase biodiversity, it is within the food supply chain that these changes will come together. Without democratising an incredibly consolidated food supply market, it will be impossible to reduce wastage, embrace innovation and change consumer behaviour. Systemic change is essential.

The way in which consumers have been educated to purchase food – both in store and in restaurants – has changed radically over the past few decades. Following significant consolidation, both retail and restaurant markets are dominated by a small number of organisations delivering a consistent and stable customer experience, one that offers products of identical size, shape and price irrespective of season or country of origin.

Of course, a sizeable proportion of fresh produce will never meet these unrealistic criteria. By creating a consumer expectation for blemish-free goods and specific size, food purveyors have built a market predicated on waste. Even if these ‘non-perfect’ items can be reallocated to sauces or ready meals, damage will occur at each stage of sorting and sifting that will result in further wastage.

Yet what has been achieved by this approach? Economically it is flawed, with subsidised agriculture and incredibly low margins for producers and retailers alike. Consumer populations – certainly in more economically developed countries – are less healthy, due in no small part to excessive consumption and the increasing use of excessive processing to address food safety concerns, especially regarding fresh food, and to extend shelf life. Yet, while much of the population feasts on unhealthy, processed food, by 2027 the world could be facing a 214 trillion calorie deficit. Something has gone awry with the global model of food production and consumption.

Over the past 50 years, the economies and ethics of food production have fallen out of sync. Farmers do not want to produce food that is wasted but every aspect of this low margin model results in wastage. Fears regarding food safety combined with failure of cold chain equipment leads inevitably to food being destroyed. But basic process failures are just one aspect of the problem.

The sheer cost of managing suppliers to ensure product consistency and safety makes it difficult for retailers to embrace new, innovative providers; whilst those with existing contracts cannot afford any risks associated with late delivery or under supply, and hence build in significant contingency. The result is not only more wastage but also minimal opportunity to invest in innovation, to explore opportunities for new, healthier food options or embrace automation to improve efficiency.

Clearly the systemic change required if the world is to avoid the predicted food crisis cannot be achieved overnight. In a difficult, low margin market, with small numbers of players fighting hard to retain share, it is incumbent upon innovators and disruptive market players to leverage digitisation to drive that change.

The most obvious role of digitisation is in minimising avoidable waste. When one in three freight journeys in the UK is food, the use of real-time information to improve routing and distribution planning is key to improving resource utilisation. In addition, using existing sensors on refrigeration units, heating units and air conditioning systems to raise alarms when problems occur to enable immediate rerouting or allocation of items, plus the use of predictive maintenance to avoid equipment downtime, can have a very significant impact on food wastage.

This approach is already being used by forward thinking organisations that are using digital and automation strategies today to reduce avoidable loss of food, achieve huge reduction in reactive maintenance costs, even reducing customer complaints. Add in the use of real-time data to support a comprehensive energy management strategy incorporating a range of different metrics, from seasonal differences to equipment reliability, and organisations can radically reduce annual power consumption. Together these changes result in a reduction in revenue expenditure of tens of millions and, in large estates, percentile point gains on capital employed can run into many hundreds.

Critically, this is being achieved by layering digitisation over existing infrastructure – clearly it is not feasible for retailers to rip and replace control infrastructure across hundreds or thousands of locations. The impact on both profit and customer experience would be hugely damaging.

Instead, by leveraging edge-based processing to ensure information from existing equipment throughout the supply chain is both actionable and actioned to make immediate changes, retailers are able to achieve IoT capacity at pace and with no downtime. It is this frictionless approach to digital adoption that will be key to releasing measurable value.

With this approach organisations can achieve a significant revenue uplift - without the need for massive investment. Indeed, it is the compelling ROI from this initial step of leveraging existing equipment that will be key to providing the investment that will underpin the next level of digitisation – the use of traceability systems to manage the advocacy, source and safety of food.

With the ability to confirm not only that products have been correctly produced but that they have followed the correct processes at every stage of the supply chain, from farm to retailer, digitisation provides a full audit trail of trusted information. This approach delivers low cost governance, radically reducing the cost of supplier ownership for retailers and opening up new opportunities for suppliers to enter the supply chain and create the democracy that is essential to enable innovation.

And it is this innovation that will be key to moving away from the entrenched practices of food procurement that have embedded consumer expectations and misunderstanding. A democracy of participation within the food market will help to educate consumers, improve understanding of food quality and the implications to health, and facilitate the introduction of new products and practices, including biodiversity, that deliver a new consumer experience.

A more predictable marketplace will also encourage investment, enabling SMEs to enter and embrace automation to replace the reliance upon cheap labour to improve productivity. The result should be not only less wastage and a fairer distribution of food globally but also a better consumer experience with access to fresher, healthier and less heavily processed food. In effect, the adoption of IoT to minimise avoidable waste within the retail cold food chain is the essential first step towards full digitisation throughout the food production lifecycle – digitisation that will underpin the global response to the developing food waste crisis.

A fundamental change to the global supply chain will take time. But there are very significant changes that can be made today that not only begin to address the wastage endemic within the food chain but also release the investment required to support the adoption of digitisation throughout the infrastructure that will be key to transforming the end to end business model.

It is by embracing digitisation to improve food safety and advocacy that the market can democratise access in order to generate the innovation key to making fundamental change, from automation to enhanced productivity to improving consumer education and supporting essential change in global food production and consumption.

There are great efficiencies to be reaped by manufacturers who are willing to incorporate the latest technological innovations into their existing manufacturing systems. The Internet of Things (IoT) has been well-documented as a likely fundamental pillar of the upcoming industrial revolution, set to upend the way we live and work. However, its applications within the manufacturing sector are limited without the involvement of artificially intelligent software.

By Chris Proctor, CEO of Oneserve.

The manufacturing industry has had a somewhat paradoxical relationship throughout history with technological innovation. In some instances, the manufacturing industry was at the forefront of developments, with inventions such as the linear assembly line driving an industrial revolution that defined the 18th century. Conversely, in recent times, manufacturing machinery has drawn a reputation for being old and cumbersome.

As a new technological era rapidly approaches, businesses are becoming acutely aware of how new software could revolutionize the way they work. It’s crucial that manufacturers look to incorporate new technologies within their systems, not least in order to stay competitive within the market, but also to make use of the vast financial and temporal efficiencies that they offer.

The Internet of Things (IoT) refers to the interconnection of devices and applications via the internet. Essentially, IoT is a comprehensive network of devices that collect and transfer data to and from one another over the internet. The most commonly used example of IoT in action is connected household appliances like smart fridges or smart energy meters, but the reach of IoT is vast and pervasive, and has particularly useful applications in the world of manufacturing.

A recent research study predicted that there would be 50 billion connected devices by 2020, putting the total global worth of IoT at $6.2 trillion. The manufacturing industry is set to contribute $2.3 trillion to this total by 2025 – a dramatic indication of the capacities these technologies have in the sector.

These devices collect data in enormous quantities, via the 'dumb' sensors embedded into them hence the name ‘Big Data’. When harnessed correctly these devices can provide extremely valuable insight for businesses on how their devices are operating.

By nature, due to the huge amount of machinery and devices that it employs, the manufacturing industry has potential access to extensive amounts of data detailing the operational capacities of each system. The problem, though, is that the data sets are so large that they are near impossible to interpret using existing processing systems, and without interpretation, they are of little use.

In short, there is a glaring discrepancy between the potential insight that manufacturers could have using the data they already hypothetically possess, and the observations that they are able to make using their current, legacy processing systems. This is where AI, or machine learning, is crucially required.

AI software, in particular machine learning programs, are able to close the gap between IoT and manufacturing by allowing businesses to better understand just how their machinery is working.

Sophisticated algorithms are able to interpret historical data sets much faster than existing systems are capable of, and in almost real-time. The analysis allows them to identify patterns and trends, which they can then use to inform later interpretation.

In essence, these algorithms are constantly 'learning' which offers an increasingly insightful interpretation over time. These algorithms are becoming so advanced that it is predicted they will eventually be able to function without any human or manual involvement, but we're still a long way from that.

Perhaps the most valuable application of AI in a manufacturing context is its ability to provide predictive maintenance. Intelligent machine learning algorithms are able to interpret historical data sets, and monitor activity to the extent that future failures can be predicted before they happen. By identifying patterns, this technology understands what the warning signs are for a potential system failure, and will alert the user to this before the failure happens, even autonomously arranging the appropriate specialist to come in and rectify the issue.

Applying AI to the vast data that is collected by a seemingly endless network of interconnected device also helps businesses make better decisions. With the analysis provided by these algorithms, businesses have tangible and sophisticated numerical evidence to support decisions that would have otherwise have to been based, at least in part, on intuition and estimation, I.e. whether a particular aspect of a manufacturing system is prohibitive in its functionality, and whether it needs to be replaced.

This has unprecedented potential in saving time and money for manufacturing companies, mostly because machine downtime is extremely costly for businesses in both financial and temporal terms. A recent research study found that machine downtime can cost businesses up to £18,000 per minute in lost productivity. Our research found that by employing predictive maintenance systems, companies can save over a third of businesses (38%) around 30 minutes per day in downtime, saving them £525,000 per year, per company. These systems have the potential to streamline efficiencies so greatly that they could reduce machine downtime almost completely.

It is clear that there are vast financial and temporal benefits to manufacturers who can not only embrace AI but link it to their existing IoT-enabled machines. However, it is also crucially important that businesses recognize just how pervasive the reach of such technologies will be in the near future. In order to stay competitive in a market that is becoming increasingly contested as manufacturing tech continues to progress, businesses must be fully aware of the disruptive potential AI and IoT have, and their capacity to define another industrial revolution.

Many businesses are sitting on a tremendous number of data sets that, when harnessed appropriately, provide a host of benefits. The analysis that is available through harnessing AI can provide businesses with discernable evidence to guide them through complex decision making, and can diminish machine downtime saving huge amounts of time and money.

Fundamentally, these benefits cannot be reaped without the application of AI. The machine learning offered by these systems provides insight and analysis that simply cannot be replicated by humans at the same level, on the same time frame. On the verge of another industrial revolution, it is imperative that manufacturers look to the potential AI has for them in closing this information void.